CBAM

Importing steel, aluminium, cement, fertilizers, electricity or hydrogen from outside the European Union is no longer a simple customs matter.

With the CBAM (Carbon Border Adjustment Mechanism), every imported tonne now entails your regulatory, financial and strategic responsibility.

It is therefore necessary to prepare and collect data, identify specific processes, and then calculate and compare results in order to optimize your declaration.MACF/CBAM

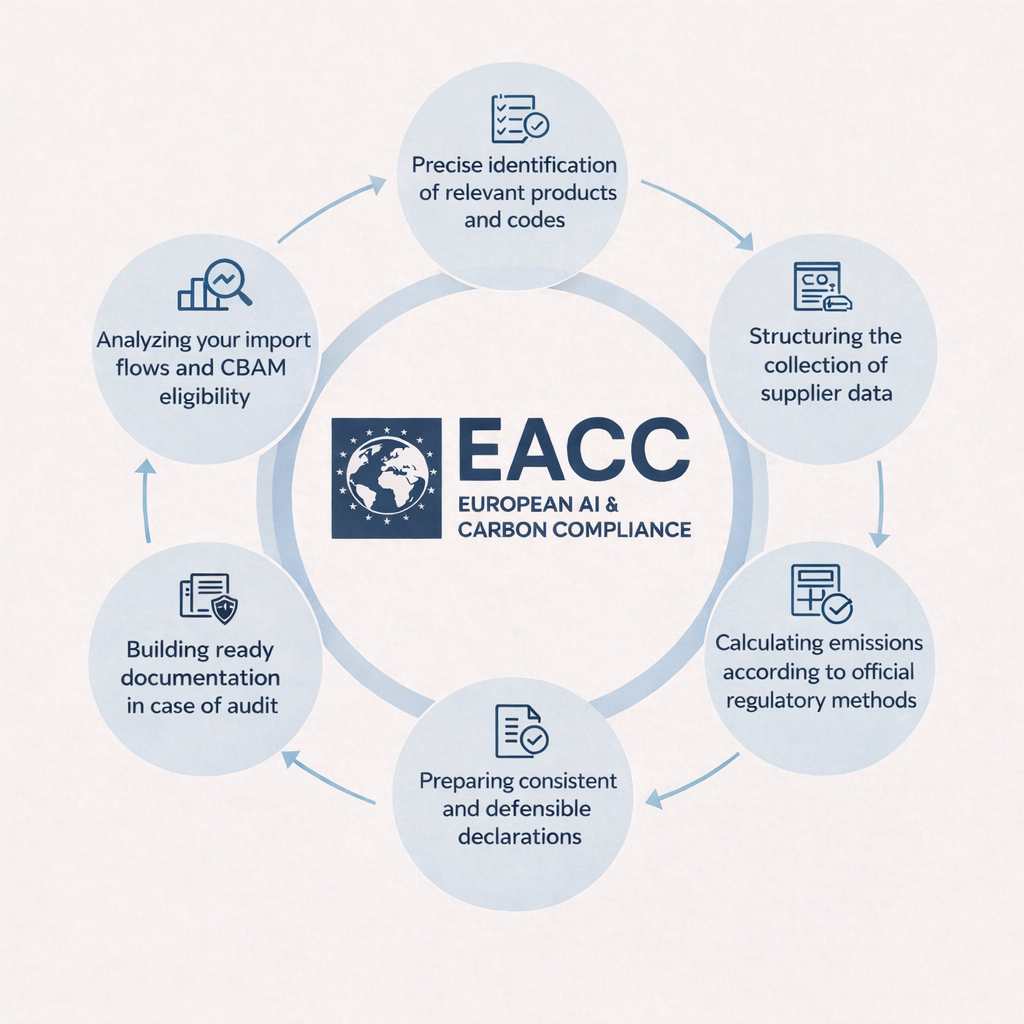

To summarize, the process should be followed step by step as follows:

Step 1: Determine whether I am subject to CBAM

First, you need to assess whether your imports are concerned.

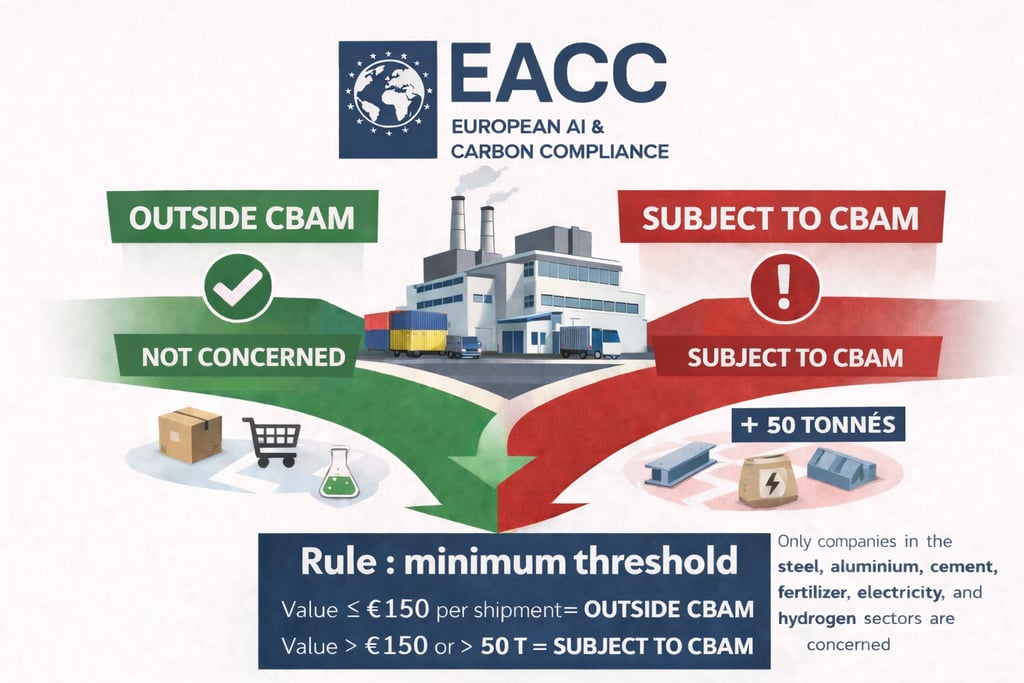

You are concerned if:

A/ The CN code of your imports appears on the European list:

This list is provided by the European Union and may be updated.

EACC supports companies in regulatory interpretation and in the CBAM classification of goods.

AND IF:

B/ The imported amount exceeds €150 or the weight of imported materials exceeds 50 tonnes (excluding electricity and hydrogen).

Subject? I am therefore considered a CBAM importer

Here are my new obligations described in the Ministry’s Simplified Practical Guide.

Step 2: Opening my CBAM Declarant Account

No later than March 31, 2026

More than 50 tonnes of imported goods planned per year?

In this case, and as mentioned in the government letter you have certainly received, you must open your CBAM declarant account.

To do so:

First, you need to go to the portal douane.gouv.fr and submit your application for authorization in the CBAM register via your ProDouane account.

Then, once the status of AUTHORIZED CBAM DECLARANT is granted, you will be able to access the CBAM REGISTER portal, called UUM&DS, which is a portal of the European Commission.

Step 3: Preparation of the annual 2026 carbon emissions declaration and payment of the tax

No later than September 30, 2027

During 2026, you must progressively prepare your annual declaration as imports are made.

The European Commission plans to make CBAM certificates available starting in 2027. These certificates will then have to be surrendered on the CBAM Register portal (UUM&DS) when submitting the annual declaration of carbon emissions generated by your goods imported in 2026.

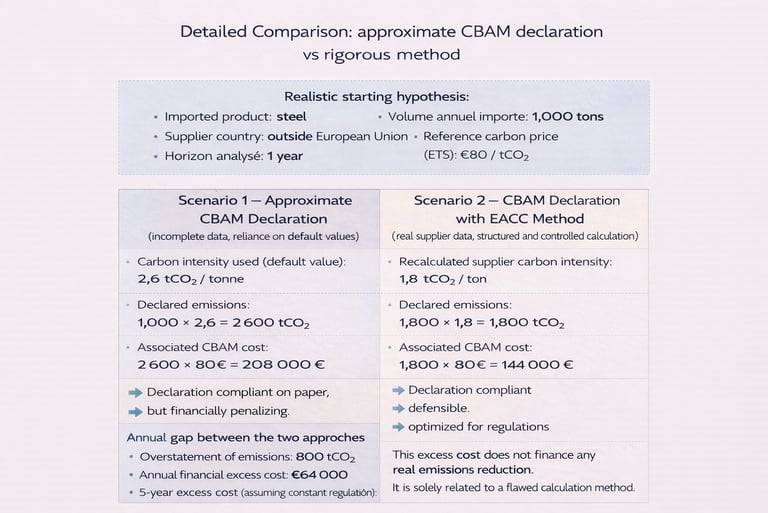

EACC is therefore here to assist you in preparing this annual declaration, as the simplified calculation of your emissions (using default values) will be disadvantageous to you. Significant preparatory work is therefore required to minimize as much as possible the cost that will be imposed on you under CBAM in September 2027.

Public documentation is available to help importers and their suppliers correctly complete CBAM declarations.

Here you will find French-language links explaining your obligations and calculation methods according to your sector:

The European Union and your country provide information

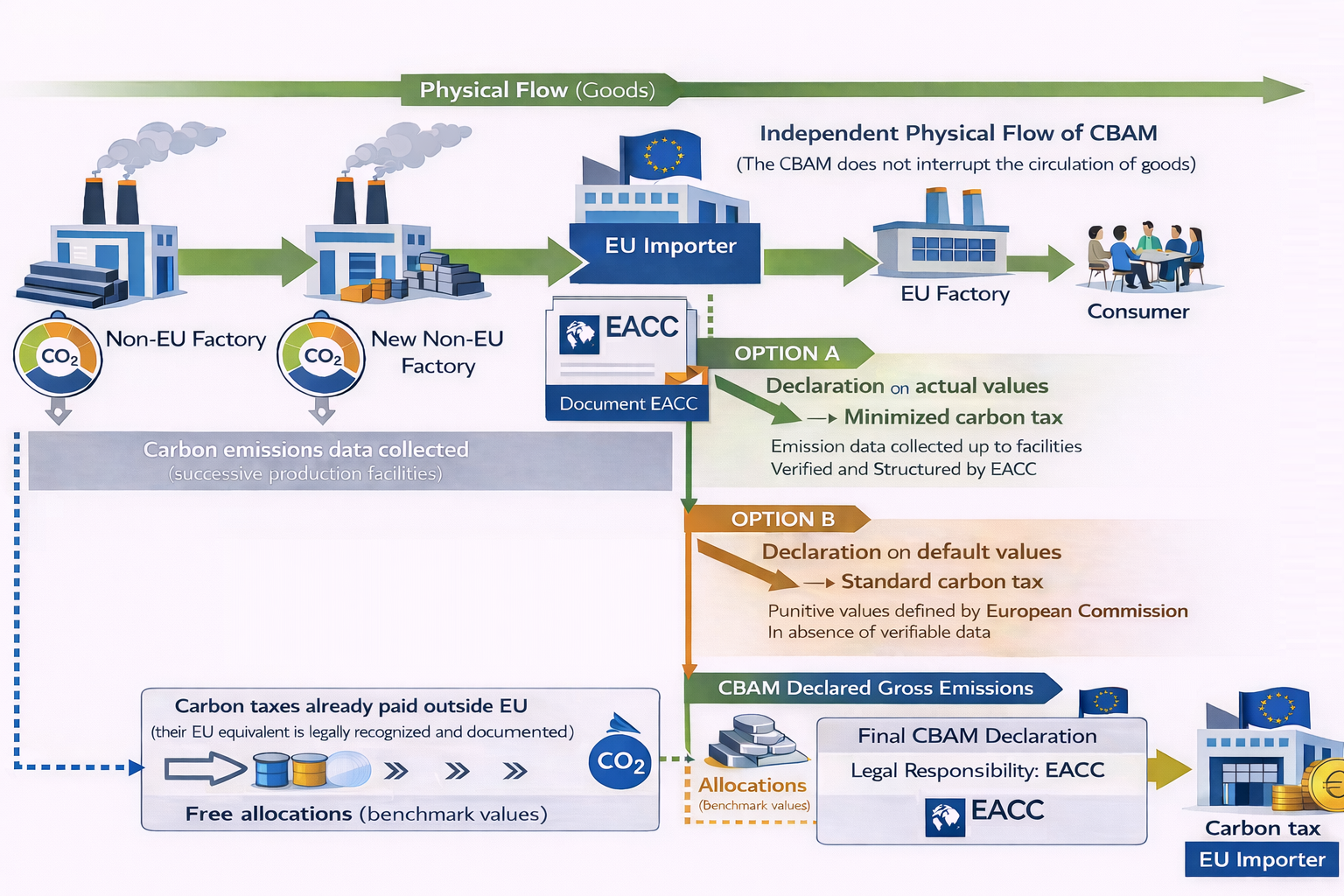

Your role is therefore to:

collect carbon data from your suppliers;

apply standardized calculation methods and choose your calculation method (Option A or B);

add variables related to free allocations and deduct carbon taxes already paid outside the EU;

then submit a complete file in order to be able to justify each declared value.

The difficulties you are facing include:

suppliers who are poorly prepared or uncooperative;

incomplete or heterogeneous carbon data;

complex and regulated calculation methods;

lack of time and internal resources;

risk of sanctions and future additional costs;

internal teams confronted with the complexity of accurate calculations.

EACC is therefore available for both options, as well as for targeted advisory support to your teams.

We take full responsibility for the technical and regulatory aspects of the CBAM

Schematic overview of the financial consequences of incorrect calculations

Key points to remember

CBAM responsibility is legal and financial.

It rests exclusively with the European importer.

Default values often result in a high CBAM additional cost.

“CBAM compliance is not an administrative formality, but a chain of technical and documentary responsibilities.”

In practice, these difficulties lead many importers to over-declare their emissions, artificially increasing their CBAM costs.

EACC Advantages

EACC acts as a technical and methodological third party, securing the importer’s CBAM declaration vis-à-vis European authorities.

Our clients choose us for:

1. Genuine mastery of CBAM calculations — not just declaration filing

Most market players focus solely on completing CBAM forms.

EACC stands out through full control of the entire emissions calculation chain, based on:

analysis of actual industrial processes;

collection, exploitation and storage of supplier activity data through our EACC ASIA Analysis Office / Data Center;

rigorous application of official regulatory methodologies, embedded and continuously updated within our internal calculation software.

Result: emissions calculated as accurately as possible, not overestimated by default.

2. Direct reduction of future CBAM costs

With many competitors, compliance is achieved at the cost of avoidable additional expenses.

Thanks to an approach based on real data rather than default values, EACC enables:

limitation of emission over-declaration;

reduction in the number of CBAM certificates to be purchased;

long-term protection of your margins.

3. Truly defensible compliance in case of audit

EACC delivers not just a declaration, but complete and structured documentation, allowing:

explanation of every calculation assumption;

traceability of data sources;

effective response to any request for justification from the competent authority.

EACC remains involved during audits, even after the declaration has been submitted.

4. Ability to work with non-EU suppliers

One of CBAM’s major weaknesses lies in relationships with foreign suppliers. This is where EACC’s strength is clearly demonstrated.

EACC benefits from an international, multilingual organization, enabling us to:

interact efficiently with suppliers outside the European Union;

structure data collection in poorly prepared environments;

transform raw data into CBAM-compliant, usable information.

5. A structured and repeatable approach over time

EACC implements a sustainable CBAM architecture, supported by continuous regulatory monitoring, allowing:

consistent declarations aligned with regulatory updates;

progressive onboarding of new suppliers through EACC ASIA;

anticipation of regulatory changes (calculation methods, benchmark values, newly impacted CN codes).

6. Independence and absence of conflicts of interest

EACC is neither a carbon broker, nor a certificate seller, nor an industrial operator.

This guarantees:

total objectivity in calculations;

no incentive to artificially overestimate or underestimate emissions;

a strictly regulatory and defensible approach;

full discretion.

7. A responsible and clearly identifiable counterpart

At EACC, accountability is clear:

an identifiable consulting firm;

documented methodologies produced by a trained and committed team;

responsibility assumed for the consistency and reliability of the delivered work.

You do not delegate your CBAM obligations to an anonymous platform or an interchangeable service provider.

Key Questions

What are the obligations for companies?

Companies must declare quarterly the carbon emissions associated with imported products and, in the long term, purchase CBAM certificates corresponding to those emissions.

When does CBAM become financially binding?

The transitional phase began in 2023 with a reporting obligation. The actual payment of CBAM certificates will start in 2027.

What are the risks in case of non-compliance?

An inaccurate or incomplete declaration may result in significant financial penalties, retroactive adjustments, and increased legal liability for the European importer.

Why are default values penalizing?

The default values set by the European Commission are intentionally high. They often lead to an overestimation of emissions and therefore a significant additional CBAM cost.

How does EACC support companies?

EACC collects and structures real supplier data, calculates emissions using a methodology compliant with the CBAM regulation, and secures the importer’s final declaration.

What is the advantage of a rigorous CBAM approach?

A rigorous approach makes it possible to legally reduce CBAM costs, secure regulatory compliance, and turn a regulatory constraint into an economic advantage.

The questions below reflect the most frequent concerns of importers facing CBAM.

“A secure CBAM declaration relies less on assumptions and more on verifiable data and a defensible methodology.

Thanks to EACC, your CBAM declaration is clear and fully under control.”

Kenneth DANO

Expert EACC

★★★★★

EACC - European AI & Carbon Compliance

For any request relating to regulatory compliance and AI Act or CBAM audits, please contact our firm.

Anthony BAUMGARTNER

Managing Director –

AI & CBAM Compliance Expert

© 2025 EACC – European AI & Carbon Compliance. All rights reserved.

EACC is a company of the Baumgartner Investissement Group, an independent French group with over 20 years of entrepreneurial experience and a share capital of €100,000.

Legal Notices

Professional civil liability: EACC carries out its consulting and audit activities within an insured framework, with professional liability insurance underwritten with Hiscox, covering regulatory compliance assignments (CBAM / AI Act).